When you see CIT Bank’s high savings rates compared to traditional banks, a natural question arises: Is this legitimate, or is there a hidden risk?

The short answer: Yes, CIT Bank is safe. It’s FDIC-insured (Certificate #35546) and backed by First Citizens Bank, one of the largest banks in the country. Your deposits are protected by the same federal protections as those of any major bank.

A Quick Comparison

| Feature | CIT Bank (Online) | Traditional “Big Banks” |

| FDIC Insured? | Yes (#35546) | Yes |

| Parent Company | First Citizens ($200B+ Assets) | Varies |

| 2026 APY Range | High (4.00% – 5.00%+) | Low (0.01% – 0.10%) |

| Physical Branches | No (Online Only) | Yes |

| Mobile Check Deposit | Yes | Yes |

The Key Facts

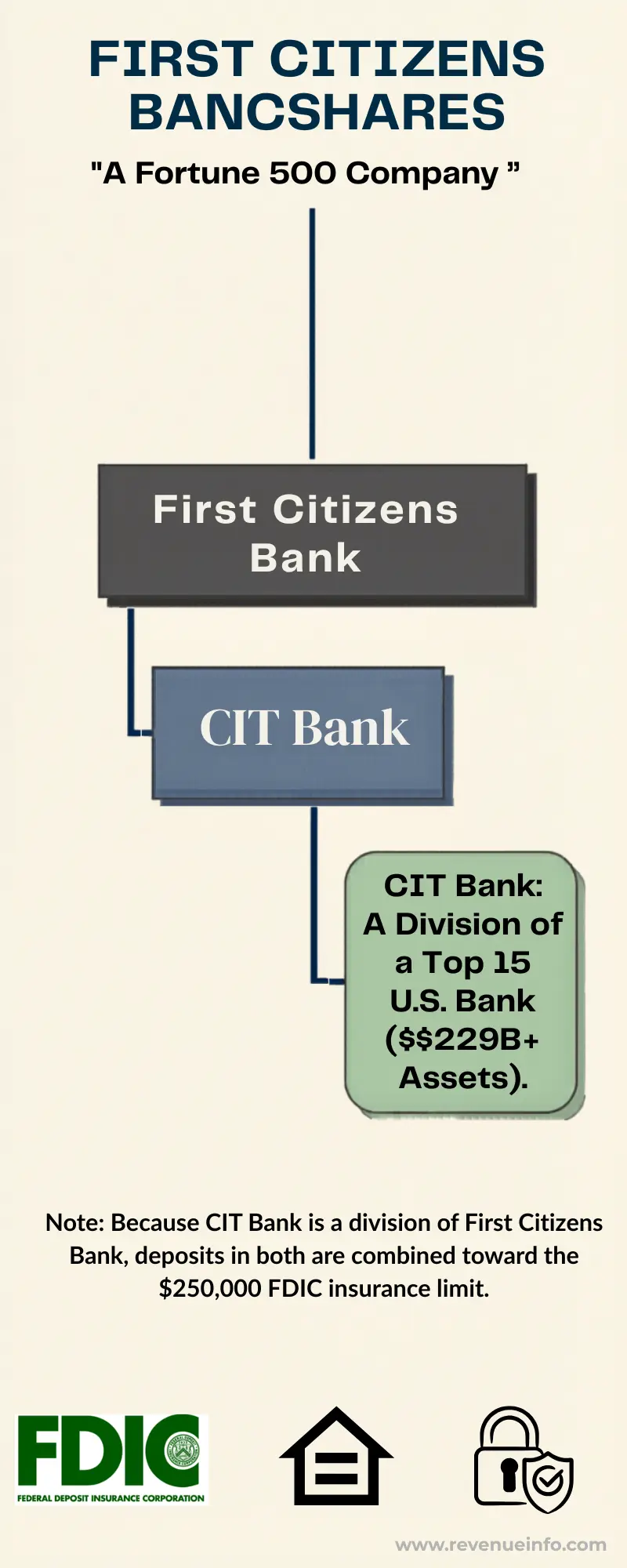

- CIT Bank operates as a division of First Citizens Bank—a Top 15 U.S. bank with over $229 billion in assets.

- Your deposits are protected by standard FDIC insurance that covers Chase, Bank of America, and every other regulated bank.

- CIT operates entirely online, which allows it to offer competitive interest rates without the overhead of physical branches.

Who Owns CIT Bank?

- CIT Bank is a division of First Citizens Bank, a financial institution operating since 1898.

- After acquiring Silicon Valley Bank in 2023, First Citizens became one of the 20 largest banks in the United States with assets exceeding $200 billion.

- This ownership structure matters because you’re depositing money with an established institution, not an independent startup.

- CIT Bank benefits from First Citizens’ capital reserves, regulatory oversight, and a century of banking experience.

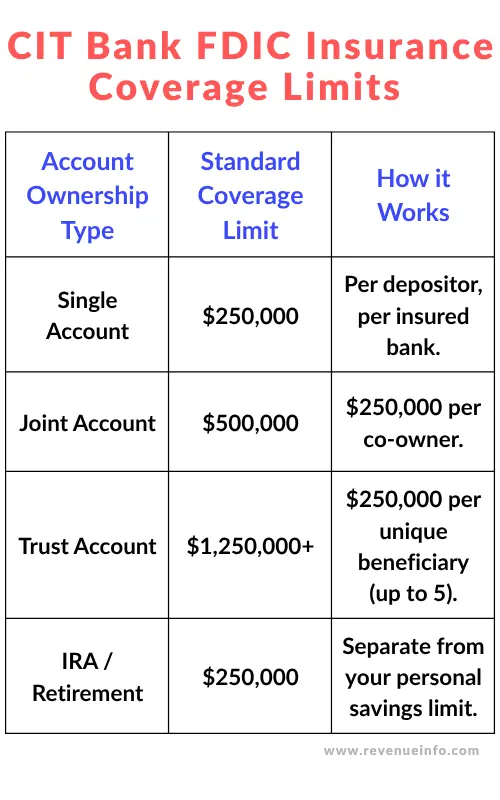

FDIC Insurance Coverage

- The Federal Deposit Insurance Corporation insures deposits up to $250,000 per depositor, per account ownership category, per insured bank.

- This protection is mandatory for U.S. banks, not optional.

CIT Bank’s FDIC Certificate Number: #35546

- You can verify this yourself using the FDIC’s BankFind tool.

Important detail:

- Because CIT Bank operates as a division of First Citizens Bank, your $250,000 FDIC limit is shared across both institutions.

- If you have $200,000 at CIT and $100,000 at First Citizens under the same ownership structure, only $250,000 total is insured.

Pro-Tip: If you open a Joint Account with a spouse at CIT Bank, your total FDIC protection automatically increases to $500,000 ($250,000 per person), making it one of the safest places for large U.S. household savings.”

What FDIC Insurance Covers

Covered:

- Checking accounts

- Savings accounts

- Money market accounts

- Certificates of deposit (CDs)

Not Covered:

- Stock investments

- Bond investments

- Mutual funds

- Crypto assets

- Safe deposit box contents

The FDIC has a 90-year track record of protecting depositors. No FDIC-insured depositor has ever lost money due to a bank failure.

Financial Stability

First Citizens Bank maintains strong capital ratios above regulatory requirements. The bank is regulated by:

- The Federal Reserve

- The Office of the Comptroller of the Currency (OCC)

- The FDIC

- State banking regulators

These agencies regularly examine the bank’s operations, lending practices, and risk management.

Digital Security Measures

- CIT Bank uses industry-standard security infrastructure:

Encryption: 128-bit SSL encryption protects all data transmission—the same technology used by major banks.

Multi-Factor Authentication (MFA): Optional secondary verification beyond passwords. Even with a stolen password, account access requires your phone or authentication device.

Biometric Login: The mobile app supports fingerprint and facial recognition.

Real-Time Alerts: Notifications for account logins, transfers, password changes, and other significant activities.

Automatic Timeout: Sessions expire after a period of inactivity.

These protocols match those used by traditional banks. Your account security at CIT is equivalent to that of branch-based banks.

CIT Bank vs. Traditional Banks: Safety Comparison

| Safety Factor | CIT Bank (Online) | Traditional Banks (Branch-Based) |

|---|---|---|

| FDIC Insurance | ✓ Full coverage ($250K) | ✓ Full coverage ($250K) |

| Federal Regulation | ✓ Fed, OCC, FDIC oversight | ✓ Fed, OCC, FDIC oversight |

| Encryption Standards | ✓ 128-bit SSL | ✓ 128-bit SSL |

| Multi-Factor Auth | ✓ Available | ✓ Available |

| Physical Branches | ✗ None | ✓ Multiple locations |

| Customer Service | Phone/online only | Phone/online/in-person |

| Account Security | ✓ Industry standard | ✓ Industry standard |

From a legal and insurance standpoint, CIT Bank and traditional banks are equally safe.

- The primary difference is physical branch access, which affects convenience but not deposit security.

Common Safety Concerns Addressed

😨Online-Only Banks Are Risky

- Online-only banks have operated for over two decades.

- Ally Bank, Marcus by Goldman Sachs, and Discover Bank are all legitimate, federally regulated institutions.

- The absence of physical branches enables higher savings rates through reduced overhead costs.

💁♂️ Customer Service Quality

- CIT Bank receives mixed reviews for customer service, with some users reporting long hold times.

- However, customer service quality is separate from deposit safety.

- Your money remains protected by federal insurance and regulation, regardless of the responsiveness of phone support.

✅Unknown Brand Name

CIT Group has operated since 1908. CIT Bank launched in 2009, making it older than many popular fintech apps. Limited advertising spending contributes to competitive rates.

CIT Bank vs. Fintech Startups

| Factor | CIT Bank | Typical Fintech App |

|---|---|---|

| Legal Status | Full FDIC-insured bank | Often just a tech platform |

| FDIC Coverage | Direct (Certificate #35546) | Partner bank (if any) |

| Regulatory Oversight | Federal banking regulators | Varies widely |

| Capital Requirements | Strict minimums | Often none |

| Years Operating | 15+ years | Often less than 5 |

| Parent Company Assets | $200B+ (First Citizens) | Often venture-backed only |

- Many fintech apps operate as technology platforms that partner with banks to obtain FDIC coverage.

- CIT Bank is a direct FDIC-insured institution, eliminating the middleman layer.

Customer Complaints Analysis

Common complaints about CIT Bank include:

- Difficulty reaching customer service

- Account verification delays

- Online-only limitations

- Transfer processing times

These complaints relate to convenience and service quality, not safety or security. There are no patterns of lost deposits, fraud vulnerabilities, or failures of FDIC insurance.

Actual Limitations of Online-Only Banking

Immediate Cash Access: Large cash withdrawals are subject to ATM limits and transfer processing times. No walk-in branch option for same-day large withdrawals.

Technology Dependence: Website or app outages prevent account access until systems are restored.

Check Deposits: While mobile deposit works for most checks, large or unusual checks may require mailing, adding processing time.

Problem Resolution: Complex issues may take longer to resolve without in-person assistance.

These are convenience limitations, not security risks.

Should You Use CIT Bank?

Safety Rating: 5/5

CIT Bank provides the same deposit security as any major U.S. bank through FDIC insurance, federal regulation, and backing from a major financial institution.

Best For:

- Managing finances entirely online

- Seeking higher interest rates on savings

- Building emergency funds or goal-based savings

- Those not requiring frequent in-person banking

Consider Alternatives If You Need:

- Regular access to large cash amounts

- Face-to-face banking relationships

- Same-day resolution of complex issues

Recommended Strategy: Use CIT Bank for high-yield savings accounts and CDs. Maintain a checking account at a local bank for everyday transactions and cash access. This combination provides competitive rates plus convenient cash access.

Bottom Line

- CIT Bank is federally insured, regulated, and backed by a $200+ billion institution.

- Your deposits are protected to the same extent as those at traditional banks.

- The choice isn’t about safety—it’s about whether online-only banking fits your financial management style and cash access needs.

Frequently Asked Questions

Is my money insured at CIT Bank?

Yes. FDIC insurance covers up to $250,000 per depositor, per account ownership category—identical to all FDIC-insured banks.

What happens if CIT Bank fails?

The FDIC protects depositors by providing immediate access to insured deposits (up to $250,000) or transferring accounts to another bank. In 90 years, no depositor has lost insured funds in a bank failure.

Can I trust an online-only bank?

Yes. Online-only banks are subject to the same federal regulations and FDIC insurance requirements as traditional banks. Physical branches don’t affect deposit safety.

How do I protect my CIT Bank account?

Enable multi-factor authentication, use a strong, unique password, monitor account activity through mobile alerts, never share login credentials, and enable biometric security on the mobile app.

Is CIT Bank better than a traditional bank?

For savings rates and online convenience, CIT often excels. For in-person service and immediate cash access, traditional banks have advantages. Many people use both types of institutions.