Buying a home is the most important financial decision you’ll ever make.

You spend months saving, but the “Credit Ghost” often ruins the finish line.

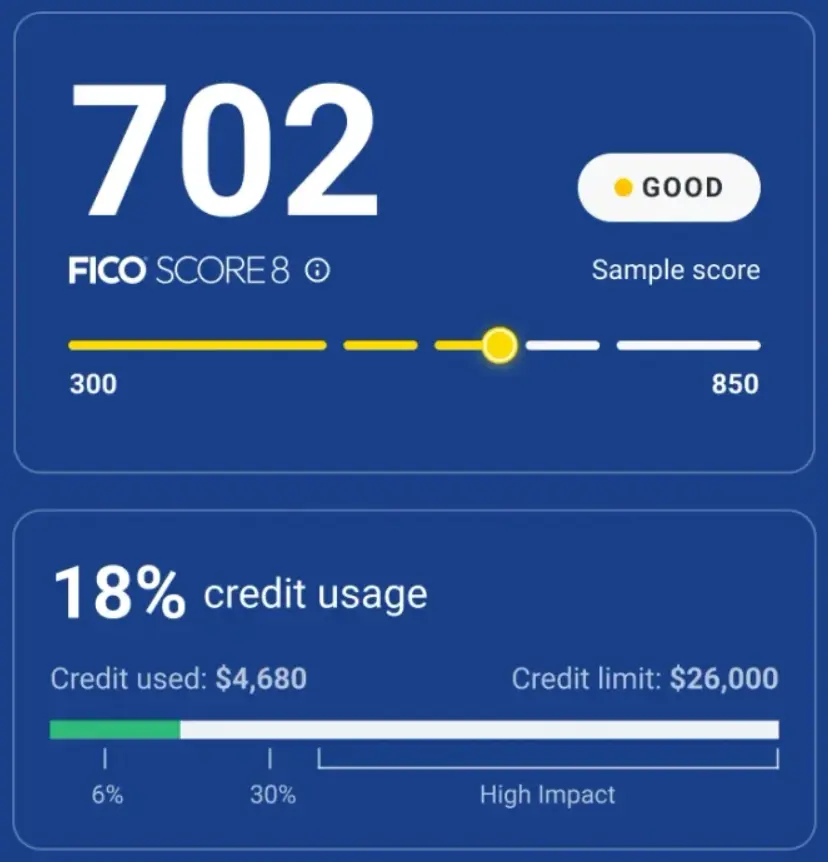

You check a generic app, see a 740, and walk into a lender’s office—only to be told your mortgage score is actually a 695.

- Why the 45-point gap?

Because in 2026, the mortgage industry will undergo its biggest shift in 20 years.

As a guy looking to enhance my credit score, I’ve tracked the transition from “Classic FICO” to the new FICO 10T and VantageScore 4.0 standards.

If you aren’t using the right apps, you’re looking at an outdated map.

Here is the definitive guide to the apps that show you what lenders actually see in 2026.

1. The 2026 Revolution: What is “Trended Data”?

For decades, credit scores were a “snapshot”—a look at your debt on one specific day. In 2026, lenders use Trended Data (the “T” in FICO 10T).

Instead of just seeing that you owe $2,000 today, lenders now see your behavior over the last 24 months.

- The “Transactor”: Someone who charges $2,000 but pays it in full every month. (Lenders love this).

- The “Revolver”: Someone who carries that $2,000 balance and only pays the minimum. (Lenders view this as higher risk, even if the score is the same).

The apps below are the only ones currently capable of showing you these specific trends.

2. Top “Mortgage-Ready” Apps (Ranked by Accuracy)

A. myFICO: The Gold Standard

- If you are within 6 months of buying, this is the only app worth paying for.

- While other apps give you a “generic” score, myFICO provides the FICO Score 2, 4, and 5—the classic versions still used for 90% of local bank approvals.

- The 2026 Edge: It now includes a FICO 10T Simulator. You can see how your trended data will look 3 months from now if you start paying more than the minimum today.

- Best For: Knowing your exact “Mortgage Score” before the lender pulls it.

- Check my FICO Score Apps for Mortgage now.

B. Experian: The Direct Bureau Powerhouse

The Experian app is a must-have because it is a direct source.

- The 2026 Edge: Experian Boost now officially counts on-time Rent and Utility payments toward your mortgage-specific scores.

- For first-time homebuyers with a “thin” credit file, this is the fastest way to bridge a 20-point gap.

Best For: Renters and those needing an instant point boost.

C. Rocket Money: The “DTI” Optimizer

Rocket Money is no longer just a budgeting app. Because it’s owned by the same company as Rocket Mortgage, its credit tool uses VantageScore 4.0, which is now officially accepted by Fannie Mae and Freddie Mac.

- The 2026 Edge: It identifies “Debt-to-Income (DTI) Killers.” It flags recurring subscriptions that might seem small but lower the total mortgage amount you qualify for.

- Best For: Cleaning up your finances to qualify for a higher loan amount.

3. The 2026 Comparison Hub: Which App to Trust?

| App Name | Score Model | Direct from Bureau? | Direct from Bureau? |

|---|---|---|---|

| myFICO | FICO 2, 4, 5 & 10T | Yes | Full 24-Month View |

| Experian | FICO 8 & 10T | Yes | High (includes Rent) |

| Rocket Money | VantageScore 4.0 | No | Yes (24-Month Trends) |

| Credit Karma | VantageScore 3.0 | No | No (Snapshot only) |

| Discover | FICO 8 | Yes | No |

Critical Warning: Do not rely on Credit Karma for a final mortgage estimate.

- It uses an older model (Vantage 3.0) that ignores the “Trended Data” lenders now prioritize.

The “Perfect” 12-Month Game Plan

If you want to secure the lowest interest rate (which could save you $50,000+ over the life of the loan), follow this schedule:

- 12 Months Out: Download myFICO and check your Trended Data. If your balances are increasing every month, stop now.

- 6 Months Out: Use Rocket Money to cancel unused subscriptions and lower your DTI.

- 3 Months Out: Use Experian Boost to ensure your rent is being reported.

- 1 Month Out: Do not open any new credit cards or buy a new car.

Final Thought:

- As a financially savvy person, I’ve learned that the person with the best data usually wins the best deal.

- Don’t go into a mortgage meeting blind. Use these tools to take control of your story.

Frequently Asked Questions

-

My score on Experian is 720, but my lender said it’s 680. Why?

You likely looked at your FICO 8 (used for credit cards), but your lender pulled your FICO 2 (Classic Mortgage). Use the myFICO app to see all 28+ versions of your score.

-

Does checking these apps hurt my score?

No. Checking your own score via these apps is a “Soft Inquiry” and has zero impact on your credit. Only when a lender pulls it for an actual loan application does it become a “Hard Inquiry.

-

I have a ‘Thin File’ (no credit history). Can I still get a mortgage in 2026?

Yes! This is the best part of the 2026 changes. By using the Experian app to report your rent and phone bills, you can generate a “scorable” report much faster than in previous years.