As you search for the best high-yield savings account in 2026, you typically come across a choice between two philosophies: the ‘tech-first’ cash management account (like Wealthfront) and the ‘bank-first’ online savings account (like CIT Bank Platinum Savings).

On the surface, the decision can seem straightforward, like—go with whoever pays the highest APY. But there is a critical trap most savers miss.

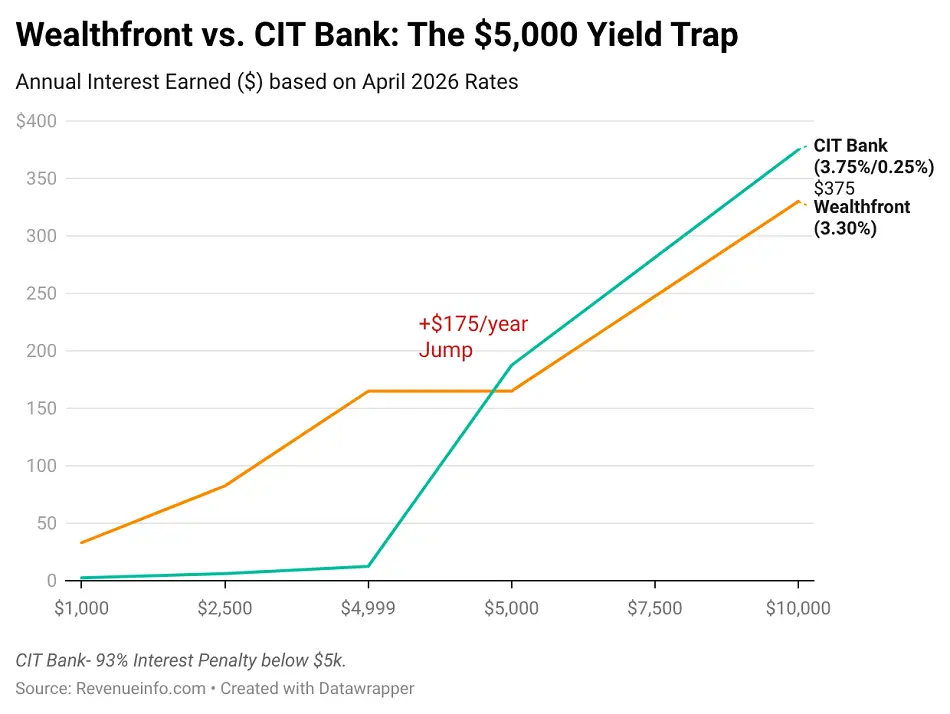

CIT Bank advertises a competitive 3.75% APY—but only if your balance stays above $5,000. Drop to $4,999, even temporarily, and your rate plummets to 0.25% which is a 93% reduction in yield.

Cit Bank vs Wealthfront Comparison: 2026 Data

| Feature | Wealthfront Cash | CIT Bank Platinum |

| APY (Base) | 3.30% | 3.75% (≥$5,000) 0.25% (<$5,000) |

| Promotional APY | 3.95% for 3 months (new users) | 4.10% for 6 months (balances >$5k) |

| Minimum Opening | $1 | $100 |

| Monthly Fees | $0 | $0 |

| FDIC Coverage | Up to $8 million | $250,000 |

| Account Features | Debit card, bill pay, mobile deposit, P2P transfers | Savings-only, limited transfers |

| Best For | Active Savers / High Net Worth, Variable balances, liquidity needs | “Set & Forget” Emergency Funds $5,000+ |

As someone who manages multiple income streams—from digital assets to real estate—I’ve learned that liquidity matters just as much as yield. A high APY (Annual Percentage Yield) is worthless if accessing your money costs you 93% of your interest.

This guide analyzes the true economics of both accounts, with particular attention to the tiered rate structure that makes CIT Bank risky for anyone with a balance near the $5,000 threshold.

The ‘Yield Trap’: Why CIT Bank Platinum is Risky for Small Savers

CIT Bank’s tiered interest structure creates what I call a ‘yield cliff’—a sharp, punitive drop in returns if your balance falls below $5,000. Here’s how it works:

The Mechanics of the Tier System

CIT Bank Platinum Savings has two tiers:

• Tier 1 (Balance ≥ $5,000): 3.75% APY

• Tier 2 (Balance < $5,000): 0.25% APY

This isn’t a gradual reduction—it’s instantaneous. The moment your balance drops below $5,000, your entire account balance earns 0.25%, not just the portion below the threshold. Consider this real-world scenario:

Scenario: You have $5,050 in your CIT Bank Platinum Savings account. You pay a $60 utility bill, bringing your balance to $4,990.

Before the withdrawal:

• Annual interest on $5,050 at 3.75% = $189.38

After the withdrawal:

• Annual interest on $4,990 at 0.25% = $12.48

👉 A $60 withdrawal just cost you $176.90 in annual interest—nearly triple the withdrawal amount. This creates a perverse incentive: you’re financially penalized for actually using your savings.

The Psychological Lock-In Effect

This tiered structure is only suitable for ‘set it and forget it’ emergency funds where you’ll never touch the principal.

For anyone who might need occasional access—whether for planned expenses, unexpected bills, or strategic rebalancing—the risk is too high. You’re not just losing interest on the withdrawn amount; you’re losing 93% of the yield on your entire remaining balance.

Verdict: CIT Bank Platinum Savings is only appropriate for disciplined savers with a stable $5,000+ balance who will not make withdrawals. For everyone else, the yield trap outweighs the APY advantage.

The Tech Edge: Why Wealthfront Wins for Liquidity and Small Balances

Wealthfront’s Cash Account operates on a fundamentally different philosophy: every dollar earns the same rate, from $1 to $8 million. There are no tiers, no minimum balance requirements beyond the symbolic $1 to open the account, and no penalty for accessing your money.

The $1 Advantage

With a $1 minimum to open, Wealthfront is ideal for:

• Those building emergency funds from scratch

• Anyone seeking a ‘free online savings account with no deposit’ requirements

• Savers who maintain variable balances due to irregular income or expenses

At 3.30% APY (base rate), Wealthfront trails CIT’s 3.75% by 45 basis points. But this gap narrows considerably when you factor in liquidity risk:

• On a $5,000 balance, the difference is $22.50 per year ($187.50 at CIT vs. $165 at Wealthfront)

• If your balance ever drops below $5,000 at CIT, even once, the annual cost swing is $164.52 in Wealthfront’s favor

FDIC Insurance: $250,000 vs. $8 Million

One of Wealthfront’s most underrated features is its extended FDIC coverage. While CIT Bank offers the standard $250,000 per depositor through FDIC insurance, Wealthfront uses a ‘bank sweep’ network that spreads deposits across multiple partner banks, extending coverage up to $8 million.

This is particularly valuable for:

• High-net-worth individuals consolidating cash from multiple accounts

• Business owners maintaining operating reserves

• Anyone uncomfortable spreading $1 million+ across four different banks to maintain FDIC coverage

The All-in-One Factor

Wealthfront blurs the line between checking and savings. The account comes with:

• Debit card and mobile check deposit

• Bill pay and peer-to-peer transfers

• No monthly fees, no minimum balance fees

This makes it suitable as a primary cash management account—you earn high-yield savings rates on money you’re actively using. CIT Bank, by contrast, is purely a savings vehicle with limited transaction capabilities.

FDIC Insurance Deep Dive: $250,000 vs. $8 Million

The difference in FDIC coverage between CIT Bank and Wealthfront represents one of the most significant structural advantages for high-balance depositors, yet it’s often overlooked in APY-focused comparisons.

How CIT Bank’s Coverage Works

CIT Bank is a single FDIC-member institution. Your deposits are insured up to $250,000 per depositor, per account ownership category. If you have $300,000 in a CIT Bank Platinum Savings account, $50,000 is uninsured. To protect the full amount, you would need to:

1. Open accounts at multiple banks, or

2. Use different ownership categories (individual, joint, trust, IRA)

This creates administrative overhead and fragments your cash across multiple platforms.

How Wealthfront’s Coverage Works

Wealthfront uses a ‘program bank’ model, partnering with up to 32 FDIC-member banks through its Cash Account sweep program. When you deposit funds, Wealthfront automatically distributes them across these partner banks in increments of $250,000 (or less, depending on account size and available partner banks).

Key mechanics:

• Each partner bank provides $250,000 in FDIC coverage

• Maximum coverage: 32 banks × $250,000 = $8 million

• The sweep happens automatically—no action required from the depositor

• You access all funds through a single Wealthfront interface

Who Benefits Most from Extended Coverage?

The $8 million FDIC coverage is particularly valuable for:

• Business owners with operating cash reserves (payroll, vendor payments)

• Real estate investors holding proceeds between property transactions

• High-income professionals building liquid reserves (doctors, lawyers, executives)

• Retirees with concentrated cash allocations from pension lump sums or asset sales

If you have $500,000+ in cash, the extended coverage eliminates the need to manage accounts at multiple institutions just to stay within FDIC limits. This consolidation reduces administrative burden and simplifies tax reporting.

The Bonus Alternative: EverBank Performance Savings

While this guide focuses on Wealthfront vs. CIT Bank, there’s a third option worth mentioning: EverBank Performance Savings. It bridges the gap between the two competitors:

• APY: 3.90% on all balances (no tiers)

• Minimum opening: $0

• FDIC coverage: $250,000 (standard)

EverBank beats both Wealthfront and CIT on base rate without requiring a $5,000 balance. However, it lacks Wealthfront’s extended FDIC coverage and checking-like features. For savers prioritizing pure yield on amounts under $250,000, EverBank is a strong contender—and will be the subject of a detailed comparison in an upcoming analysis (EverBank vs. CIT Bank).

The Final Verdict

The choice between Wealthfront and CIT Bank isn’t about which account has the higher advertised APY—it’s about which structure aligns with your liquidity needs, balance stability, and risk tolerance.

Choose Wealthfront Cash Account if:

• Your balance is under $5,000 or fluctuates near that threshold

• You need liquidity and don’t want to worry about yield cliffs

• You want an all-in-one cash management account with a debit card and bill pay

• You have high balances ($500,000+) and want extended FDIC coverage without managing multiple banks

• You’re building savings from scratch and want to earn full interest on every dollar from day one

Choose CIT Bank Platinum Savings if:

• You have a stable emergency fund of $5,000+ that you will not touch

• You want the absolute highest yield and can commit to maintaining the balance threshold

• You’re comfortable with a traditional bank structure and don’t need checking features

• You already have a separate checking account and want a dedicated savings vehicle

The Bottom Line

For most American savers—especially those with balances under $10,000 or anyone who values flexibility—Wealthfront’s no-tier structure and extended FDIC coverage make it the safer choice. The 45-basis-point APY difference is a rounding error compared to the risk of accidentally triggering CIT’s yield trap.

However, if you’re a disciplined saver with a fixed $5,000+ emergency fund and no liquidity needs, CIT’s 3.75% APY (or 4.10% promotional rate) is difficult to beat. Just remember: the moment your balance drops below the threshold, you lose 93% of your yield. Make sure the juice is worth the squeeze.

As someone who manages income streams ranging from digital assets to land, I’ve learned that liquidity is a hidden cost. The best high-yield savings account isn’t the one with the highest advertised APY—it’s the one that pays you well without penalizing you for being human and occasionally needing your money.